Does Urgent Care Take Insurance? What Every Patient Needs to Know

Yes, urgent care takes insurance. If you are asking does urgent care take insurance, the answer is yes — most clinics accept major plans. However, your cost depends on whether your clinic is in-network. This guide tells you exactly what to expect before your visit.

Medically reviewed by Sean Parkin, PA — CEO & Founder, CityHealth

Does Urgent Care Take Insurance? Yes, Most Clinics Do

Most urgent care clinics accept major plans. That includes Aetna, Blue Cross Blue Shield, Cigna, United Healthcare, Medicare, and Medicaid. However, the key factor is whether the clinic is in your plan’s network. So while urgent care does take insurance in most cases, your cost depends on your specific plan and the clinic you choose.

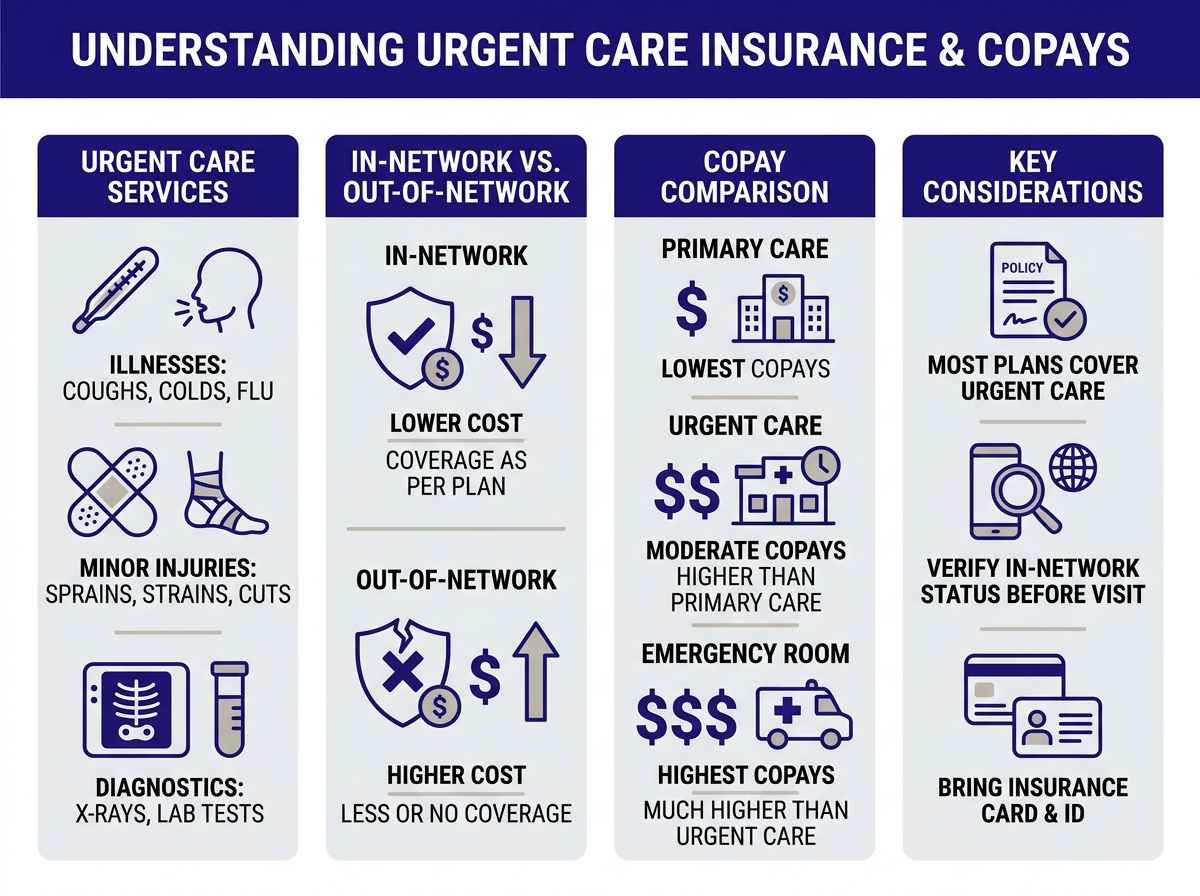

Urgent care sits between a primary care office and an ER. Because of this, most insurance plans treat urgent care visits as covered benefits. Your plan almost certainly includes urgent care coverage. The goal is to confirm in-network status before you walk in.

In-Network vs. Out-of-Network: Why It Matters

Your insurer sets discounted rates with specific clinics. Those clinics are “in-network.” When you visit one, you pay your plan’s copay or coinsurance. As a result, the visit costs much less than out-of-network care.

Out-of-network clinics have no contract with your insurer. Your plan may still pay part of the bill. However, your share is higher — sometimes much higher. Some plans pay nothing for out-of-network urgent care outside of emergencies. Therefore, always check network status before you visit.

The Healthcare.gov glossary on in-network benefits explains how cost-sharing works and why network status matters.

What You Pay With Insurance at Urgent Care

Your cost depends on your plan. Most in-network visits use a flat copay or a coinsurance rate. Either way, the cost is far below an ER bill. For example, the average ER visit costs $1,500 or more. An in-network urgent care visit typically runs $20 to $150. For a full breakdown, see our guide on urgent care copay costs.

Copay vs. Coinsurance

A copay is a flat fee you pay at the visit. For example, your plan might charge $40 for urgent care, no matter what services you get. Coinsurance works differently. Instead of a flat fee, you pay a percentage of the allowed cost. If your rate is 20% and the visit allowed amount is $200, you pay $40. Your insurer pays the rest.

Some plans use both. You pay a $30 copay for the visit, then owe 20% on any lab tests or X-rays ordered that day. Because of this, read your Summary of Benefits for your specific urgent care terms before your visit.

Which Insurance Plans Does Urgent Care Accept?

Most established urgent care clinics accept these major plans:

- Aetna — widely accepted nationwide

- Blue Cross Blue Shield — accepted across most state plans

- Cigna — in-network at thousands of locations

- Humana — accepted at many walk-in clinics

- Kaiser Permanente — usually requires Kaiser facilities

- Medicare — Part B covers urgent care as an outpatient service

- Medicaid / Medi-Cal — accepted at participating clinics; call ahead

- Tricare — covers active-duty members and dependents

- United Healthcare — widely accepted, including UHC Community Plan

However, even if your insurer is on this list, coverage depends on the specific clinic. Therefore, always call or check the insurer directory before visiting.

Does Urgent Care Take Insurance for Physicals?

This depends on your plan. Some urgent care clinics offer sports physicals, school physicals, and employment physicals. However, insurance treats physicals differently from sick visits. Most plans and Medicare cover one annual wellness exam per year. If your physical qualifies as preventive, your plan may cover it with no copay. Because plan rules vary, call your insurer first to confirm how physicals at urgent care are covered.

Does Urgent Care Accept Out-of-State Insurance?

Most of the time, yes. National plans like Aetna, Cigna, BCBS, and United Healthcare cover you in any state where the clinic is in-network. As a result, your coverage follows you when you travel. However, regional plans work differently. A Medi-Cal plan covers California residents in California only. Out of state, you may only have emergency coverage. Therefore, check your plan’s out-of-area benefit before traveling.

Does Urgent Care Bill You Later With Insurance?

For most visits, you pay your copay at check-in. The clinic then bills your insurer for the rest. You owe nothing more for services your plan covers fully. However, you may get a follow-up bill in some cases. For example, if the clinic orders lab work or imaging, those may bill as separate claims. In addition, if you haven’t met your annual deductible, you pay the full allowed amount until your deductible is met. Ask the front desk whether additional services will bill separately. This one question prevents billing surprises.

How to Verify Your Coverage Before You Go

Five minutes of prep can save you hundreds of dollars on your visit. Follow these steps:

- Call your insurer. Ask if the clinic is in-network.

- Check the online directory. Most insurers have a search tool on their website or app.

- Call the clinic. Ask which plans they accept. Contracts change, so verify directly.

- Bring your insurance card. The front desk verifies eligibility in real time before you see a provider.

What If You Don’t Have Insurance?

Urgent care is still available without insurance. Most clinics offer self-pay rates much lower than billed amounts. A basic sick visit typically costs $100 to $200 cash. Some clinics also offer payment plans. For full pricing details, see our guide on the cost without insurance. Also note that Medi-Cal enrollment through Covered California is open year-round. You could enroll and use coverage on the same day, because income-based eligibility is verified quickly.

CityHealth San Leandro Accepts Most Major Insurance Plans

CityHealth urgent care in San Leandro accepts Aetna, Blue Cross Blue Shield, Cigna, United Healthcare, Medicare, and Medi-Cal. Our team verifies your coverage at check-in so you know your cost before you see a provider. We treat a wide range of conditions — from sick visits and infections to physicals, labs, and X-rays. See the full list of conditions we treat to confirm we can help with your concern.

CityHealth accepts Aetna, Blue Cross Blue Shield, Cigna, United Healthcare, Medicare, Medi-Cal, and more.

Walk in at 201 Dolores Ave, San Leandro, CA 94577 — no appointment needed. Mon 10am–7pm, Tue–Fri 9am–7pm, Sat–Sun 9am–5pm.

Frequently Asked Questions

- How much does urgent care cost with insurance?

- With in-network insurance, most patients pay a copay of $20–$75. Some plans use coinsurance (typically 15–20%) instead of a flat copay.

- Does urgent care take Medicaid?

- Many urgent care clinics accept Medicaid, but not all. Call ahead to verify, since acceptance varies by location and state.

- Does urgent care bill you later with insurance?

- Typically no — you pay your copay at the visit. However, if additional services are ordered, you may receive a bill after your insurance processes the claim.