You’re sitting in your car outside an urgent care clinic, staring at your insurance card, wondering what your urgent care copay will actually be. You’re not alone. In fact, thousands of patients each week face the same question before walking through the door. The good news: a copay at urgent care is almost always lower than an ER visit, and knowing what to expect can save you real money.

Medically reviewed by Sean Parkin, PA — CEO & Founder, CityHealth Urgent Care

What Is an Urgent Care Copay?

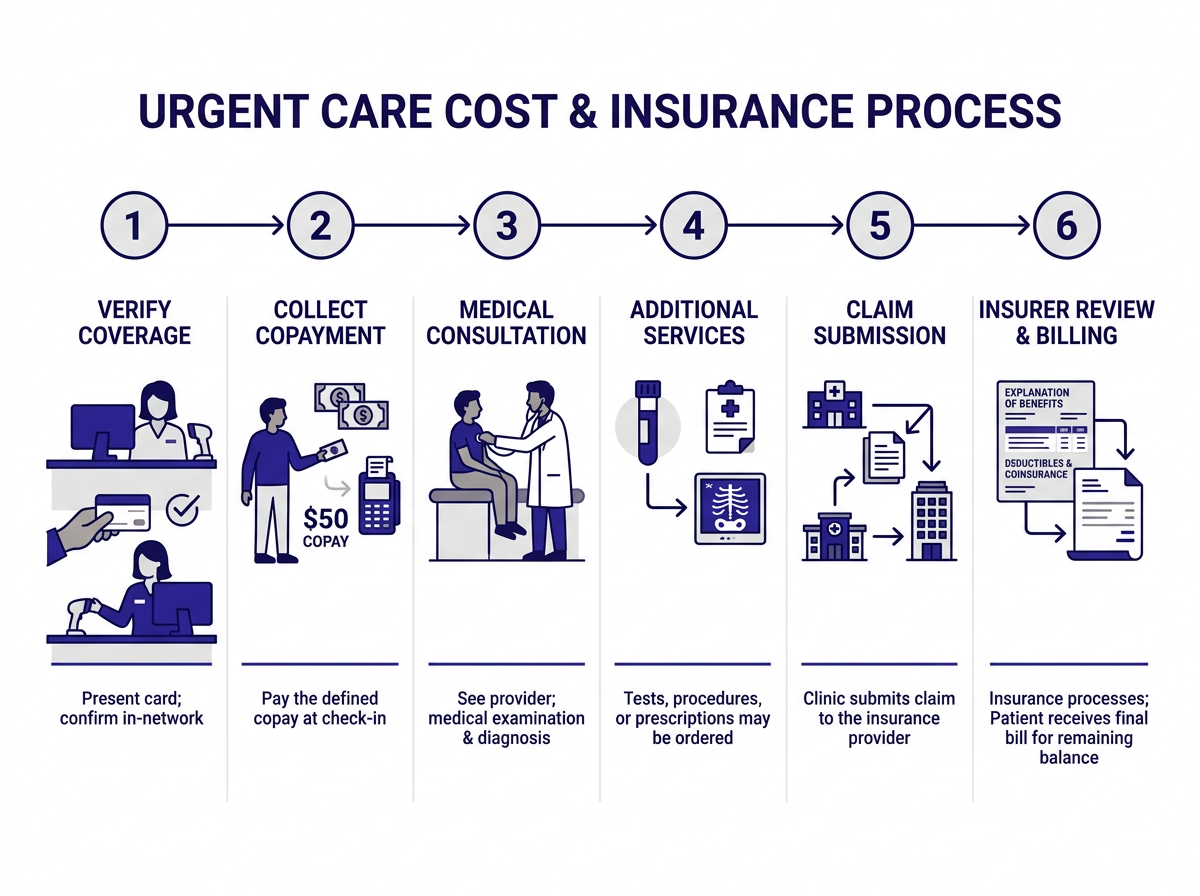

A copay is a fixed dollar amount you pay at the time of your visit. Your insurance company sets this amount when you enroll in your plan. For most insurance plans, the urgent care copay ranges from $25 to $75 per visit. In other words, this is the amount you owe regardless of what tests or treatments you receive during that visit.

However, copays are not the only cost you might face. Depending on your plan, you may also owe coinsurance (a percentage of the total bill) or have a deductible to meet first. For example, some high-deductible health plans (HDHPs) require you to pay the full cost of care until your deductible is met. In that case, your copay structure kicks in only after you hit that threshold.

Because every plan is different, always check your Summary of Benefits before your visit. You can usually find this document on your insurer’s website or app. It lists your copay for primary care, urgent care, specialists, and emergency room visits in a simple chart.

Urgent Care Copay vs. Emergency Room Copay

One of the biggest reasons patients choose urgent care is cost. Specifically, the difference between a copay at urgent care and an ER copay can be significant.

Here is a typical comparison:

- Primary care office visit copay: $20 to $40

- Urgent care copay: $25 to $75

- Emergency room copay: $150 to $500 or more

In addition to the copay gap, ERs often charge facility fees that can push your total bill into thousands of dollars. Urgent care clinics typically do not charge these extra facility fees. As a result, your total out-of-pocket cost at urgent care stays much lower, even if additional services like X-rays or lab work are needed.

According to Healthcare.gov, a copay is your share of costs for a covered healthcare service. Therefore, knowing where your plan sets each copay tier gives you direct control over what you spend.

How to Find Your Urgent Care Copay Before You Go

Fortunately, you do not have to guess. Here are four ways to confirm your copay before your visit:

1. Check your insurance card. Most cards print copay amounts on the front or back. Look for a line that says “Urgent Care” or “UC.” If your card only shows “Specialist” and “PCP,” your copay at a walk-in clinic usually matches the specialist tier.

2. Call the number on the back of your card. Similarly, a representative can tell you your exact copay, whether you have a deductible to meet first, and whether the clinic you plan to visit is in-network.

3. Log in to your insurer’s website or app. Most major carriers (Blue Cross, Aetna, UnitedHealthcare, Kaiser) let you look up benefits online. Then, search for “urgent care” in the benefits section to find your copay amount.

4. Ask the front desk. Walk-in urgent care clinics verify insurance daily. The staff at check-in can run your insurance and give you an estimate before you see a provider. At CityHealth, we do this for every patient so there are no billing surprises.

What Affects Your Urgent Care Copay Amount?

Several factors determine what you pay at an urgent care visit. Consequently, understanding these factors helps you plan ahead and avoid unexpected bills.

Your plan type matters. HMO plans often have lower copays but require referrals. PPO plans offer more flexibility but may charge higher copays for out-of-network visits. EPO and POS plans fall somewhere in between. Because plan structures vary, two patients with the same insurer can have very different copays.

Network status is critical. If the urgent care clinic is in your plan’s network, you pay the contracted rate. On the other hand, if it is out-of-network, you may owe more, or your visit may not be covered at all. Also, some plans treat out-of-network visits differently when you are traveling versus at home.

Your deductible status plays a role. If you have a high-deductible plan and have not met your deductible yet, you may pay the full negotiated rate for the visit instead of just a copay. Once your deductible is met, the copay applies. For this reason, early-in-the-year visits tend to cost patients more.

Common Services Covered Under Your Urgent Care Copay

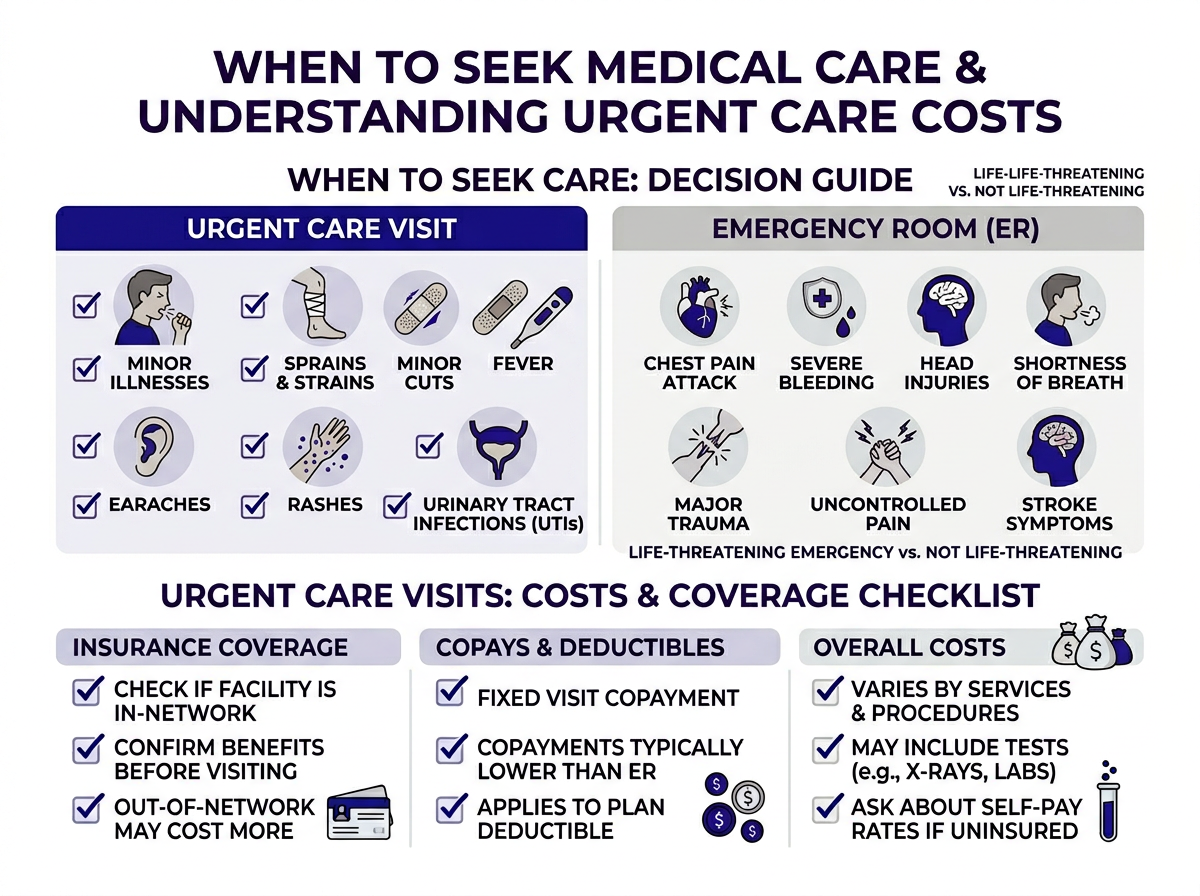

Most urgent care visits fall under your standard copay. However, some services may trigger additional charges. Below is what typically falls under the copay and what might cost extra:

Usually covered by your copay alone:

- Provider evaluation and diagnosis

- Basic wound care and stitches

- Strep tests, flu tests, and COVID tests

- Prescription writing

- Follow-up instructions and referrals

May incur additional charges:

- X-rays and imaging

- Lab panels (blood work, urinalysis)

- Splints, casts, or orthopedic supplies

- Procedures like abscess drainage or foreign body removal

These extra charges usually fall under your coinsurance or count toward your deductible. Therefore, it helps to ask your provider upfront what tests they plan to order so you can understand the full cost picture.

What If You Don’t Have Insurance?

If you are uninsured, you will not have a copay structure. Instead, you pay the self-pay rate for your visit. Even so, many urgent care clinics, including CityHealth, offer transparent self-pay pricing that is still far below what an ER charges.

For example, a typical self-pay urgent care visit costs between $100 and $300 depending on the services needed. An ER visit for the same condition can run $1,500 to $3,000 or more. Because of this gap, urgent care is often the best option for uninsured patients who need same-day treatment.

You can learn more about options at CityHealth in our guide to urgent care without insurance and our breakdown of urgent care costs without insurance.

Tips to Keep Your Urgent Care Copay Low

You have more control over your healthcare costs than you might think. With that in mind, here are proven strategies to minimize what you pay:

Stay in-network. Above all, this is the single most effective way to keep your copay low. Before choosing an urgent care clinic, verify it is in your plan’s provider directory.

Use urgent care instead of the ER for non-emergencies. Conditions like sprains, minor cuts, ear infections, UTIs, and flu symptoms are treated faster and cost less at urgent care. For more on this, read our comparison of urgent care vs. emergency room costs.

Ask about bundled pricing. Additionally, some clinics offer flat-rate packages for common visits. This can be helpful if you have a high-deductible plan and are paying the full negotiated rate.

Bring your insurance card and ID. Otherwise, missing documentation can delay verification and sometimes result in being billed at the self-pay rate, which you then have to appeal.

Go early in the day. This is not about cost, but shorter wait times mean less time away from work. That has its own financial value.

Your Urgent Care Copay at CityHealth

At CityHealth Urgent Care in San Leandro, we accept most major insurance plans. As a result, our front desk team verifies your coverage and confirms your copay before you see a provider. We believe in transparent pricing with no surprise bills.

We are a walk-in clinic, so you do not need an appointment. However, you can reserve a time to reduce your wait. In addition, we treat adults and children for a wide range of non-emergency conditions, from sore throats and rashes to fractures and lacerations.

Ready to get care today? Book your visit online or walk in during business hours. Our team will handle the insurance details so you can focus on feeling better.